How I'm Paying-Off $18,000 of Student Loan Debt in 9 Months

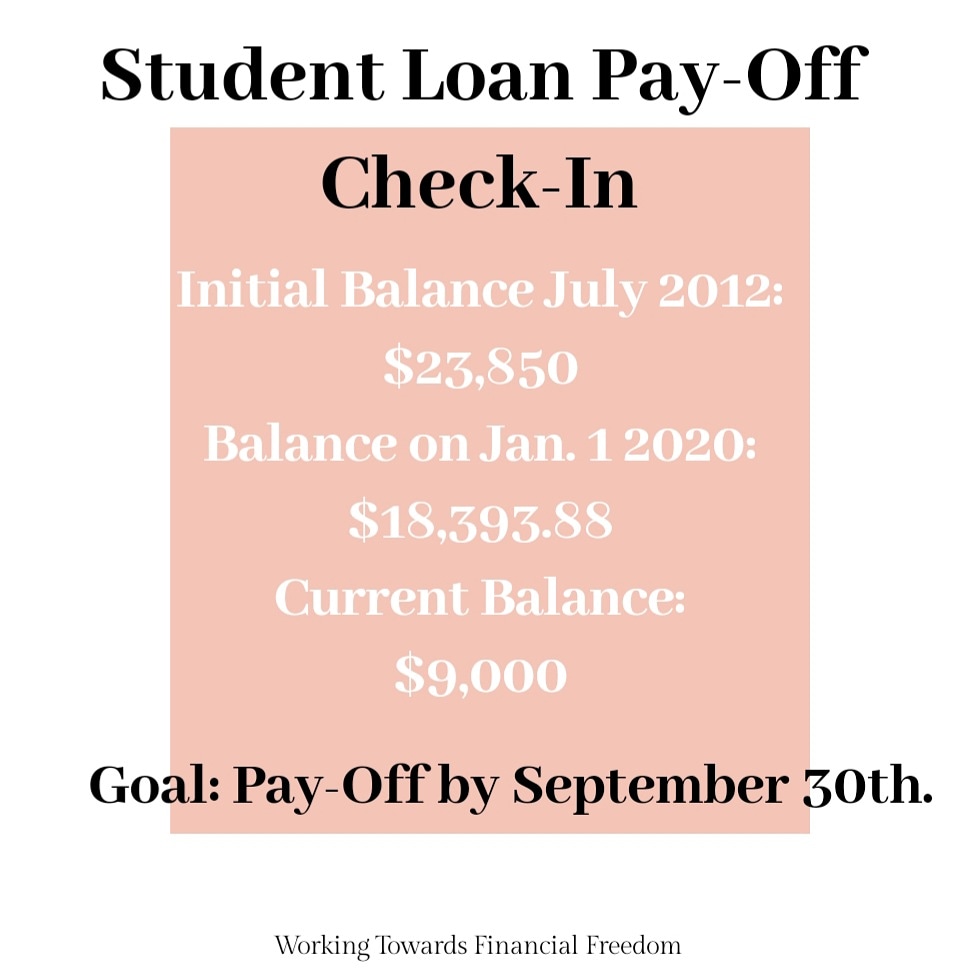

I received my Master’s degree in May 2012. It had been a long journey. I went to school part-time, mostly online with a few in-person classes, as I worked full-time. I was so excited. I was finally done. No more long nights finishing reading assignments or turning down invitations to hangout because I had a paper due. I felt free! Then reality hit. I was now on the hook to pay back $23,850 with a 6.8% interest rate. Yea, the Fixed Interest Rates for Direct Subsidized Loans and Subsidized Federal Stafford Loans for Graduate or Professional Borrowers between July 2006 and June 2012 was 6.8%.

When the first bill arrived 6 months later (In case you didn’t know most federal student loans give you a 6-month grace period after you graduate, leave school, or drop below half-time enrollment to get financially settled and to select your repayment plan.), I treated it just as such. Another bill to add to the list. Make the required payment, on time of course (I didn’t want to mess up my credit score. If you haven’t had the chance check out my post on credit scores.) and move on. I didn’t put much more thought into it than that.

Then tax time came and I realized only about half of the $3,000 I paid towards my graduate student loan that year came off of the principal. The other half went to paying the interest!

I Felt Deflated

Instead of feeling motivated to do something about this, I felt deflated. What was the point? I was never going to be able to make a noticeable dent in this debt. It just was what it was. I mean everyone has student loan debt, right? According to an American Progress report, about 43 million Americans—roughly one-sixth of the U.S. population older than age 18—currently carry a federal student loan. Besides wasn’t Student Loan Debt good debt? I used these arguments to help justify and ultimately accept that this debt would be with me forever. Deciding I would rather focus on other debts to eliminate like my undergraduate student loan that had a much lower interest rate and I could see substantial changes to the balance, and my personal loan which had a significantly lower balance, so I could see an end in sight.

But eventually my thought process changed (in case you missed it, here’s why I decided to finally ditch my student loan debt in 2020) and I had to come up with a plan to ditch this debt.

I Paid More in 6 Months than I Had in 8 Years

I couldn’t believe it, but it just goes to show what you can accomplish when you’re determined. I had done in 6 months what it had taken me 8 years to do. Now to be fair there were a lot of factors at play. During that 8 years, I had made changes to put myself in the position to be able to do this.

I moved closer to my job, which saved a little money on my commute.

I eventually moved into a cheaper place and saved a couple hundred bucks on rent.

I had paid-off other debts, freeing up money once used for bills.

I cancelled or re-negotiated subscription services.

I padded my savings as much as I could.

And to be frank, I was making a lot more money after receiving several promotions throughout the years.

All of these steps had financially prepared me for what I was about to do.

My Plan to Pay-Off $18,000 in Student Loan Debt in 9 months

The plan was simple:

Make larger payments. I decided I would cut what I was putting away into my savings by half and use that money towards my student loans.

Make additional payments. I figured to do this I would either have to bring more money in or reduce the amount of money going out. This turned out to be a little easier than expected. In April I received a pay increase! And due to the “shelter-in-place”, my monthly expenses had dropped quite a bit. No more paying for commuter parking ($104 per/month). No more temptations to hit-up Pret-a-Manger on my way to work. No more happy hours or dining out (even though I do miss doing this) or just grabbing lunch at a nearby eatery when I forgot or didn’t feel like bringing my own. You never realize how quickly these expenses add up until you no longer have them. Long story short, my disposable income was increasing and I knew exactly where I was going to dump it.

Use any additional funds received. I put my entire $811 tax refund and the unexpected $200 stimulus check I received towards my student loan.

Use a portion of my savings. I know some people frown against doing this, but after doing the math to me it made sense. At the time, the interest rate on my savings account was about 1.20% and the interest rate on my student loan was 6.8%, meaning that the amount of money I would make by keeping this money in my savings would be a lot lower than the money I’d end up owing in interest to my student loan if I didn’t. So, with that being said I decided to use $5,500 of my savings to wipe out the largest portion of the debt.

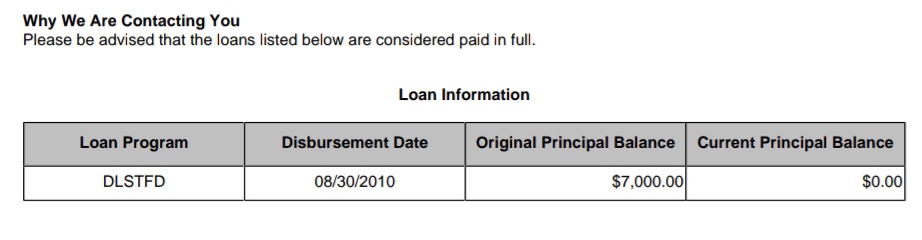

Balance on February 29, 2020

And it felt really good when I received this.

Then, as if the skies opened and a light shined down on me, the interest rate on federal student loans had been reduced to 0%, thanks to the CARES Act. I couldn’t believe it. Due to the CARES Act, I decided I needed to pay-off this loan by September 30th. Meaning the $9,000 that I still owe is all I would actually have to pay-back.

If you are currently on your own journey to pay-off student loans let me know how it’s going in the comments. Or, if you’ve already paid-off your student loans, (Firstly, Congrats!) and let us know how the journey was for you.

Also, be sure to stay tuned as I will revisit this topic in late September to let you all know whether I met my goal or not. In the meantime, you can follow me on Instagram (wtff_finance) where I’ll give monthly updates.

I just got so excited reading this! I'm so happy for you! I know you will reach your goal! You appear to be the type of person that won't let anything get in the way of their goal!

ReplyDeleteKudos to you! And thank you for walking me through this! I want to reach financial freedom sooner rather than later. And I'm sure this blog will definitely help me achieve this goal!

Thanks! :-)

DeleteI'm happy for you!! Also thanks for the detailed post. Will be helpful to me at some point ❤️

ReplyDeleteThanks V! This definitely will be you one day :-)

DeleteThis is a super exciting one! I recently paid off all my student debt recently through saving and being savvy. So it's so nice to see how other people are doing it! X

ReplyDeleteAwesome Kayleigh! And thanks for the comment. Can't wait until this debt is officially paid-off!

DeleteGood luck with your debt free journey! I'm currently hoping to be completely debt free by March 2021 and am following Dave Ramsey's debt snowball method x

ReplyDeleteRoni | myelevatedexistence.com

Thanks Roni! I too am a fan of the snowball method. Good Luck on your journey!

DeleteThis was a good post. I like how you broke everything down and how you even added the charts and stuff in there. It really gave a better visual of what you were talking about. And showed that little by little you got it down.

ReplyDeleteThanks Ez! Yes, I think sometimes visuals can be very helpful in getting your point across.

DeleteAwesome blog post! I've been wanting to start paying off my student loan debt before it gets out of hand, definitely taking some of these suggestions!

ReplyDeleteWow, I really needed to read this! I’m definitely in that mindset that I’m going to die with student loan debt. I just need to get it together! Super helpful as always .

ReplyDeleteLOL I think we are all under that mindset at some point and time after we graduate and are hit with these massive bills. It took me a very long time to decide it was time to be done with this debt and started taking steps to make a plan to pay it off. But just as I did, you can too! And as always thanks for the comment! :-)

DeleteThis is such a great post - I'm so keen to ditch my student loan debt asap!

ReplyDeleteCarrie xx

www.redwritesabout.com